Content

All of the cash sales of inventory are recorded in the cash receipts journal and all non-inventory sales are recorded in the general journal. Journal entries are the backbone of all financial reporting. As such, transactions must be verified and the corresponding journal entries cross-checked for accuracy. Whether the books are completed manually or digitally, credits and debits on affected accounts must be allocated according to standard accounting rules. Sales returns and allowance are the contra account to the sales revenues where the previously recognized sales need to be derecognized by recording into this account.

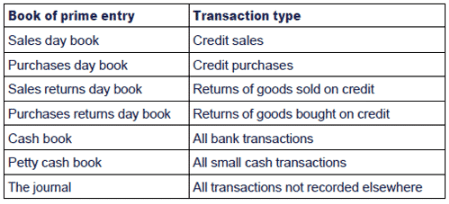

The accepted, standard practice is to use a double-entry accounting system, which generally entails the use of both a general ledger and a general journal. It can also include the use of special journals for frequent transactions within a specific category. An expense accrual refers to an expense reported in an accounting period before it is actually paid. An example is electricity used by a plant in the month before the utility issues a bill for the company to pay. It’s crucial to accurately enter complete journal data so that the general ledger and financial reports based on this information are also accurate and complete.

How To Record A Credit Sale

In the merchandising business, we may need to sell merchandise on account in order to increase the sale volume we can make each year. The general journal is used for adjusting entries, closing entries, correcting entries, and all transactions that do not belong in one of the special journals.

- Conversely, this creates an asset for the seller, which is called accounts receivable.

- We’re here to take the guesswork out of running your own business—for good.

- ; therefore, it will come in the Assets side of the balance sheet under current assets.

- So a typical sales journal entry debits the accounts receivable account for the sale price and credits revenue account for the sales price.

- This is a common practice, and the discount may differ from one company to the next depending on the terms and conditions.

- The hospitality industry is highly competitive and requires a strategy to earn and retain a customer’s business.

The example below also shows how postings are made from the sales journal to both the subsidiary and general ledger accounts. Each individual sale is posted to its appropriate subsidiary account. After the posting, the account number or a check is placed in the post reference (Post Ref.) column. Likewise, the inventory balances at the end of the accounting period will be based on the actual physical count of inventory. At the same time, the cost of goods sold during the period will be calculated by using the beginning inventory plus purchases minus the ending inventory. The total of cost of goods sold & inventory column is debited to cost of goods sold account and credited to inventory account in the general ledger.

What Is A Journal Entry?

In the case of accounting periods, the closing entry reflects the ending balance for that account at the end of that accounting period. That value is then transferred as the opening entry for the next accounting period. In that case, it is the accounting period for that account, which is closed. MyToys Manufacturing Co. buys $100,000 worth of raw materials. It pays $10,000 in cash and uses credit for the balance. The company would record a debit, or increase, of $100,000 in raw materials. The Cash account would show a credit, or decrease, of $10,000 because that was the amount paid in this transaction.

Markup refers to a price increase while markdown is a price decrease by amount or percentage. Learn how to calculate markups and markdowns, explore a t-shirt business example, and discover ways to manage special event pricing. You can’t just erase all that money, though—it has to go somewhere. So, when it’s time to close, you create a new account called income summary and move the money there.

Shipping On Sales

Entering transactions in the general journal and posting them to the correct general ledger accounts is time consuming. In the general journal, a simple transaction requires three lines—two to list the accounts and one to describe the transaction. The transaction must then be posted to each general ledger account. If the transaction affects a control account, the posting must be done twice—once to the subsidiary ledger account and once to the controlling general ledger account. To speed up this process, companies use special journals to record repetitive transactions that affect the same set of accounts and have a consistent description. Such transactions can be documented on one line in a special journal.

The customer does not receive a discount in this case but does pay in full and on time. Credits sales together with cash sales and installment sales compose the net sales of the entity, which is found in the income statement.

Modern accounting software negates the need for special journals by making it easy to sort transactions and search for granular details. Reversing entries are made at the beginning of a new accounting period and serve to reverse, or undo, an adjusting entry made at the end of the previous accounting period. This option provides a significant reduction in accounting errors due to double-counting expenses or income and increases efficiency in processing actual invoices in the new accounting period. In other words, they are used to simplify bookkeeping. These entries record more than one account to be debited or more than one account to be credited. The rule of journal entry requires the total of debits and credits to be equal, but the number of credits and debits do not have to be equal. For example, there may be one debit but two or more credits, or one credit and two or more debits, or even two or more credits and debits.

This increases Sales Returns and Allowances and decreases Cash. CBS does not have to consider the condition of the merchandise or return it to their inventory because the customer keeps the merchandise. On September 1, CBS sold 250 landline telephones to a customer who paid with cash. On September 3, the customer discovers that 40 of the phones are the wrong color and returns the phones to CBS in exchange for a full refund.

Still, the accounting treatment for both the transactions is the same, and mostly the same account is used to record both types of transactions. On Feb 5, journal entry to record the sales return and the buyer’s account adjustment.

Perpetual Inventory System

The first step is to determine if the entity is selling goods or services. Record the journal entries for the following sales transactions of a retailer. The chart in Figure 6.12 represents the journal entry requirements based on various merchandising sales transactions. In the first entry on September 1, Cash increases and Sales increases by $37,500 (250 × $150), the sales price of the phones. In the second entry, COGS increases , and Merchandise Inventory-Phones decreases by $15,000 (250 × $60), the cost of the sale. On August 1, a customer purchases 56 tablet computers on credit. The payment terms are 2/10, n/30, and the invoice is dated August 1.

A sales journal entry is the same as a revenue journal entry. Transfer money from an asset, liability, or equity account to an income or expense account. These entries mark the end of an accounting period at a balance that can then be transferred from a temporary account to a permanent one, or from one accounting period to the next. In the case of temporary accounts, the closing entry zeros out the account, and any balance above that is transferred to another, more permanent account. The purpose of a journal entry is to physically or digitally record every business transaction properly and accurately. If a transaction affects multiple accounts, the journal entry will detail that information as well.

Here is the entry to recognize inventory and derecognition of the cost of goods sold. Now we have to deal with inventory/goods that customers just returned. These two journal entries are generally booked simultaneously, as one action drives the need to book both of them. Assuming we use the perpetual inventory system and the merchandise’s original cost is $3,000 in our inventory record. On October 10, the customer discovers that 5 printers from the October 1 purchase are slightly damaged, but decides to keep them, and CBS issues an allowance of $60 per printer.

Compound Entries

No manually inputting journal entries, thinking twice about categorizing a transaction, or scanning for missing information—someone else will do that all for you. Will decrease; therefore, sales on account journal entry the total balance of current assets will not remain the same. An expense is incurred for the cost of goods sold, since goods or services have been transferred to the customer.

- Accurate and complete journals are also essential in the auditing process, as journal entries provide detailed accounts of every transaction.

- A reduction to Accounts Receivable occurs because the customer has yet to pay their account on October 10.

- The Cost of Goods Sold account, and expense account, is debited for the same cost as the inventory was recorded at, as shown below.

- We will need to keep the returned goods in the company’s warehouse and reflect this transaction correctly in the accounting records.

- There are six types of journal entries, or seven if you count the archaic, vague and seldom-used single entry.

- Each individual sale is posted to its appropriate subsidiary account.

The $30 is recorded when the client makes the first payment. The other three payments are not recorded until each is made respectively. The cash accounting method is the simplest way to keep track of actual financial status. In this method, you don’t account for the sale until the cash is collected. After collecting the cash, you add the amount received as a credit in the ledger. If a sales tax liability is created by the sale transaction, it is recorded at this time, and will later be eliminated when the sales tax is remitted to the government. One may also ask, how do you record a journal entry for sale of inventory?

You will have to decide if you are going to tackle some or all adjusting entries, or if you want your accountant to do them. If your accountant prepares adjusting entries, he or she should give you a copy of these entries so that you can enter them in your general ledger. Accounts receivable is the balance of money due to a firm for goods or services delivered or used but not yet paid for by customers. On account is used in accounting to note partial payments or purchases made on credit.

North American Morning Briefing: Stock Futures -2- — Morningstar.com

North American Morning Briefing: Stock Futures -2-.

Posted: Mon, 29 Nov 2021 10:53:00 GMT [source]

Sales can be cash or have credit terms using Accounts Receivable since we will receive money from the customer in the future. To record sales, we will debit Cash or Accounts Receivable, depending on payment, and credit Sales Revenue. Lastly, review the trial balance to make sure the journal entry posted to the correct ledger corresponds with the correct dollar amounts. Assuming the company making the sale is actually a service organization, that pays employees to perform services for a fee, the accounting is a little different. In the event that certain inventory is consumed and used in the process of providing the service, this will be recorded as part of Cost of Goods Sold as the previous journal entry shows. However to account for the cost of paying the employee that is providing the related services, the company will need to determine what the cost of these employees is. AccountDebitCreditCash$$$Accounts receivable$$$The journal entry for cash received from the sold merchandise on account is the same for both the perpetual inventory system and the periodic inventory system.

Sales returns occur when a customer returns goods to the seller due to some fault, while the term sales allowance is used when the buyer agrees to keep the products, but for a lesser price. On Feb 2, the journal entry to adjust inventory and record cost of goods sold account. Show the general entries to record sales and sales return in the books of ABC cosmetics. On 2nd Feb 2020, the firm recorded credit sales of 10 pieces for product Y and 15 pieces for product Z to one of its old customers for $50 and $25 each respectively. Businesses make their money by selling goods or services. The revenues brought in drive all other transactions, therefore the proper recording of those sales is essential in the bottom line coming out to an accurate number. For example, on September 1, we make a $5,000 merchandise sale on account to one of our customers.

What is the difference between sales journal and sales ledger?

Information is recorded in journals in chronological order by individual transaction, which makes it easier to sort through information and find the specific items that users need. Information is recorded in a ledger in a number of accounts, which are typically sorted in the following order: Asset accounts.

Likewise, the inventory balances will be up to date and the company can review it anytime without making physical inventory count. Of cause, the company still performs the physical count of inventory sometimes for the control purpose. Your general ledger is the backbone of your financial reporting.

A debit is entered as a negative figure, but the end result is an increase to your returns and allowances balance. When goods or services are sold to a customer, and the customer is allowed to pay at a later date, this is known as selling on credit, and creates a liability for the customer to pay the seller. Conversely, this creates an asset for the seller, which is called accounts receivable. A general journal is a book of raw business transactions recorded in chronological order by date.

- CBS determines that the returned merchandise can be resold and returns the merchandise to inventory at its original cost.

- Post the general journal totals to the general ledger.

- As we know, the customer returns the goods to the company.

- If it were the credit sales, then we should credit to the account receivable account.

- On September 1, CBS sold 250 landline telephones to a customer who paid with cash.

- Accounts Receivable decreases and Cash increases for the full amount owed.

Therefore, the return increases Sales Returns and Allowances and decreases Accounts Receivable by $3,500 (10 × $350). The second entry on October 6 returns the printers back to inventory for CBS because they have determined the merchandise is in sellable condition at its original cost. Merchandise Inventory–Printers increases and COGS decreases by $1,000 (10 × $100).

Author: Kevin Roose